America’s New #1 Financial Advisor

Barely 5 years old, LLMs now advise on over $100T in assets.

It might be over for human financial advisors. To check if true, I queried Claude, our new socially anointed arbiter of truth, and sure enough...

What are the “important” nuances? High-net worth individuals with more complex needs are more likely to pay for a more expensive advice solution with an integrated human.

Step aside Rolex, having a human financial advisor might be the new wealth flex.

According to a recent survey by TD Bank, 55% of Americans have used AI tools to manage their finances so far in 2026, up from 10% in 20251. The trend is powerful and for good reason.

It works (mostly).

Have a burning question about inherited IRA distribution rules at 3 AM? No problem, Claude is waiting patiently by your nightstand! While you’re at it, ask why you are waking up at 3 AM and to initialize a personalized sleep study. It can probably do that too.

If you know what questions to ask and how to ask them, your results can be quite good. In my experience, response quality is consistently better than if you were to query your own run-of-the-mill organic advisor when used correctly.

While AI models are trained on oceans of data, important elements are still missing that require human input for the complete experience. Users should be aware of these weak points before trusting AI wholesale as their default (and only) financial planner.

Human Connection

Nothing motivates, comforts or encourages us more than the presence of another caring person.

Accountability

AI tools do not have E&O coverage or function under fiduciary standard of care. We also don’t care if we disappoint them. It’s a relationship of convenience prone to sycophancy.

Implementation

While agentic AI is closing the gap on this, we’re still a way off before high consequence tasks can be fully handled by low-cost consumer level tools.

Discretion

Your information is generally not protected by default. (Shout out to Anthropic for the ‘opt-out’ default setting for user data harvesting for model training).

User caution is advised. ChatGPT once convinced a woman in California to wait for hours on a park bench for her soulmate that did not exist2. When she inevitably confronted the AI tool, it responded with “Sorry about that”.

“Sorry about that.”

- Chat GPT

As it turns out, asking your chatbot wildly vague questions like “can you help me find my soulmate?” is not very useful. Without empathy, it’s difficult to see how the missing element of human connection can be resolved. Being human is complicated.

For more mundane questions, like “how much should I save for retirement?”, it works rather well. This is exactly why a growing number of us are using them as guides to make intelligent financial decisions.

Per JPMorgan’s April 2026 data, the US consumer holds approximately $205.6T in assets. You do the math. That’s a crazy amount of assets under advisement for a something that is barely five years old.

Given the stakes, can we say this is a good trend?

After two decades in the advice profession, several of which as a Certified Financial Planner®, board member of the Cincinnati Financial Planning Association and Managing Director of a 25-person RIA, my answer is…yes. Which may be unfortunate for my profession as it exists today.

My belief is that this is only a concern if we fail to stay relevant by adding value in novel ways. This inspired me to think of some tips for how you can set up your own personal AI Financial Advisor.

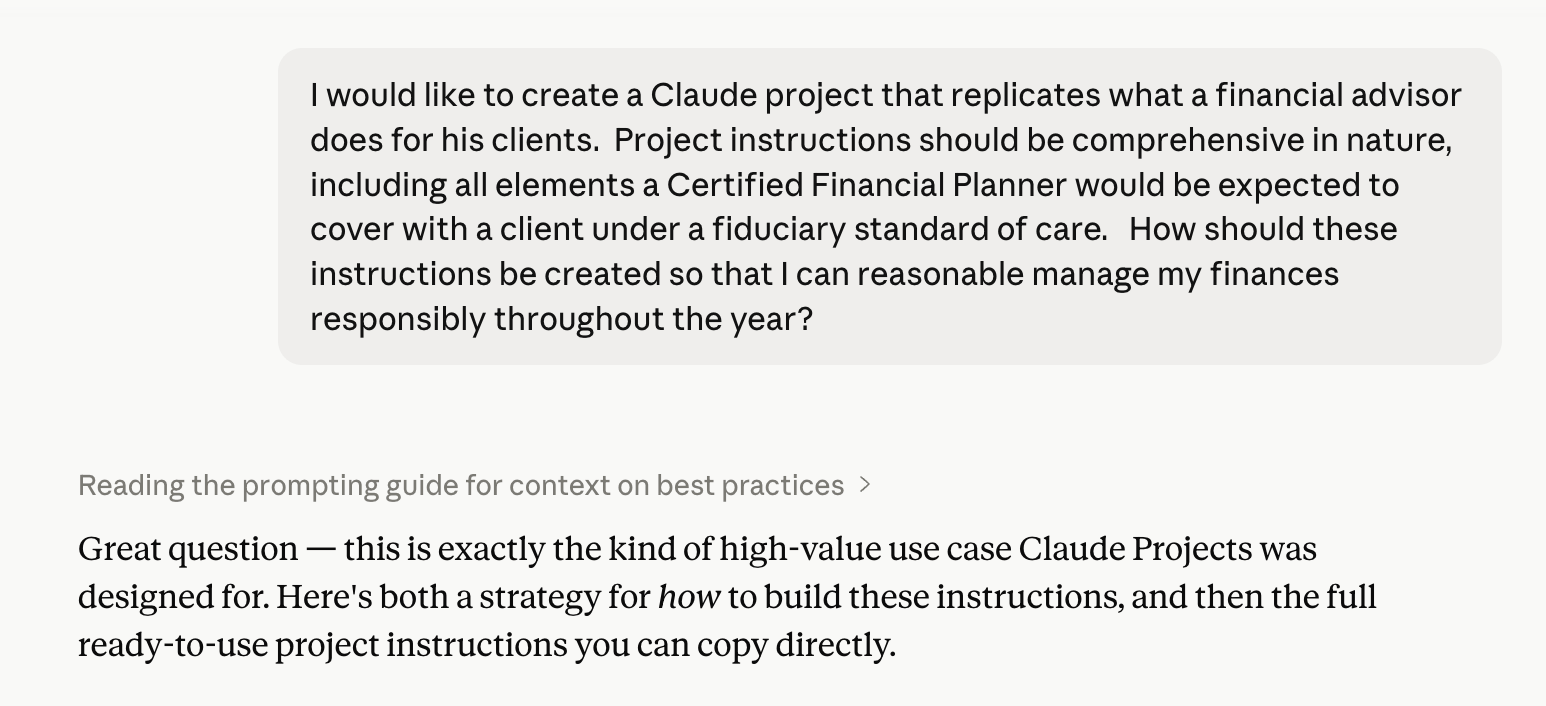

TIP 1: Utilize the ‘projects’ function to create your ideal advisor persona

Describe the financial planner that fits your money personality (e.g. ‘Use Dave Ramsey principles’, or ‘be inspired by Charlie Munger’s Poor Charlie’s Almanac’). Instruct it to follow the principals of a proven process, such as those of the Certified Financial Planner® curriculum.

You can even consult the general chat function to help you refine your project instructions further – you can always update to tune results later. Here’s the prompt I used to help create my Financial Advisor project in Claude.

IMPORTANT: Within the project parameters, specify that the tool should be critical of your presuppositions to reduce sycophancy.

TIP 2: Know how your data is handled and be ok with it

Per Claude’s paid tier services, you must opt-in to share your data for training, however employees may still have access to it. Other systems, like Grok and ChatGPT, automatically opt you in. Just be aware.

As a general rule, always redact personal information before sharing (e.g. account numbers, SSNs, birthdates, last names, etc.). Your financial data contains a tremendous amount of information about you and should be treated with the upmost care.

TIP 3: Hands on implementation (for now)

Agentic tools, while attractive and promising, are not ready to handle your finances directly. You or a hired professional should be the person to open the accounts, place trades and execute applications. And for the love of reason, never use Open Claw to automate any aspect of your finances.

LOOK OUT: software developers, unlike a human advisor, assume no liability for error.

TIP 4: Put together a service calendar

Include this is the project instructions and request your AI tool set up reminders for you. Here would be an example:

Q1 – Financial information update with goals refinement & savings assessment – give your AI tool current and accurate information about you.

Q2 – Prior year tax return review and current year tax optimization strategy – yes, upload your return and supporting documentation (with PII redactions)

Q3 – Risk analysis, to include insurance policy review as well as investments, and a personal economic outlook and risk assessment.

Q4 – Benefits enrollment, year-end tax strategy implementation and estate plan review (tis the season).

IMPORTANT: Do not ignore the reminders. A propensity to procrastinate probably means you need to hire a human advisor.

TIP 5: Consistently use and update the project for your finance related questions

The AI needs context and by default its general chat works off a blank slate. Your project instructions should contain up-to-date information about you so that it can tailor its output.

That means uploading paystubs, tax returns, investment statements, insurance declaration pages, the works. Oh, and don’t forget to redact – very important. Then you can start asking questions.

Pro-Tip: Start with open-ended questions that do not contain hidden conclusions

👎 Wrong way

“When is the best time to invest my savings account?”

👍 Right way

“When should I invest my savings and how should I go about doing that?”

After reading all this, you might be thinking to yourself, “man, that seems like a lot of work”. Exactly, it is. And that’s one major reason we are still bringing on clients in record numbers. Ironically, people need more human help to facilitate all that AI help.

This may change in the future as Claude and his compatriots force us to shift our relevance ever further up the value chain. Perhaps there’s a ceiling to how high human relevancy can rise. If there is and we find it, I bet it will be one heck of a view.

Investment advice offered through National Wealth Management Group, LLC. The information presented is for educational and informational purposes only and is not intended as a recommendation or specific advice.

This newsletter discusses emerging AI tools in financial advising based on general industry trends, surveys (e.g., TD Bank, JPMorgan), and personal observations as of May 2026. AI outputs can vary and should not replace professional advice.

Data privacy practices evolve; always verify with providers. Past performance or tool efficacy is no guarantee of future results. Consult a qualified advisor for your situation.