Behind the Collapse of SVB

What the bank's failure means for you.

It’s rare that financial news is so exciting that it breaks through the usually more colorful regular news cycle, but we live in unusual times. Headlines have been pasted all over the landing pages or the major news outlets opining on the collapse of Silicon Valley Bank headquartered in Santa Clara, CA. I’ve read many. Some are tediously accurate while others trigger the GFC engrained fight or flight response. Bank closures due to failure are unfortunately not uncommon. In fact, we usually see 3 to 4 banks fail every year. What makes the SVB failure more salient is that it was the 16th largest US bank, and more importantly, it was the primary bank for more than 50% of the startups in country. The failure hits innovative entrepreneurs and venture capitalists right where it hurts. These people tend to live high-profile lives that catch the attention of the media. Under normal circumstances, this would be hum drum “move along folks, nothing to see here” news, but not so today. You should care because Twitter says so.

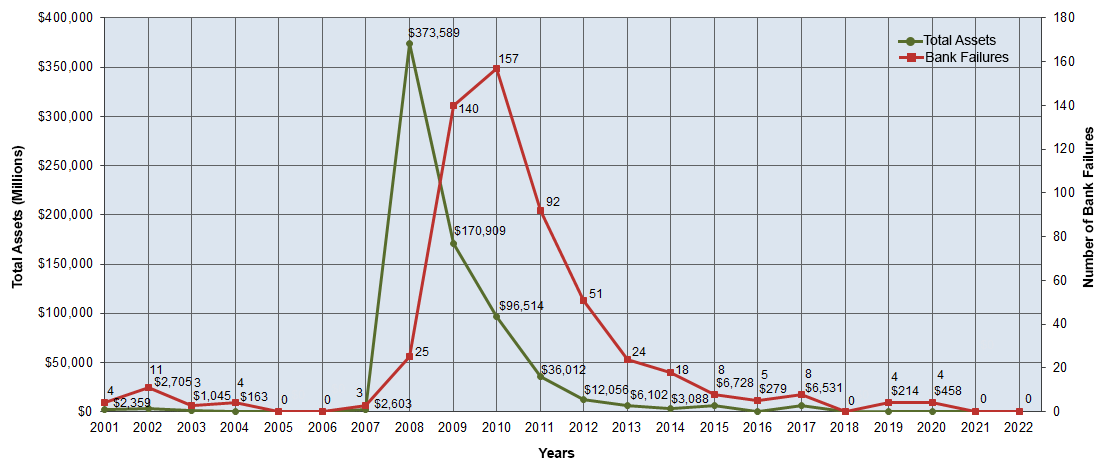

Source: https://www.fdic.gov/bank/historical/bank/

Since the media has done the hard work of grabbing your attention, allow me to take the laser pointer to walk us through what exactly happened. Believe it or not, it isn’t that complex. To fully grasp the cause, you need to have a cursory understanding of interest rate risk . This is the inherent secondary market risk of holding a bond through time as interest rates change. The longer the time frame and the greater the change in interest rates, the greater the risk as a measure of volatility (spikes up and down). Think of bonds like a teeter-totter: on one side you have rates and the other price. As rates rise, price falls and vice versa. The reason behind this is the same reason your cell phone carrier buys your old phone as a trade in at a reduced cost. Everyone wants the improved newer phone (including yourself, hence the trade-in), so your old phone is worth less in the resale market. Now, let’s apply this principle to a bond; you bought a 10-year bond with 1% annual coupon three years ago but now the ‘improved’ newer bonds yield 4%. No one wants to buy your old bond in the secondary resale market so you must either 1) sell the bond at a fraction of what you bought it for to attract buyers, or 2) hold the bond until it matures which could be a long time.

We’re still in the anger induced finger pointing stage so the official blame for the SVB collapse has yet to fall on anyone’s head. To me, the facts as seen today point to a massive failure of competence on the part of SVB’s management. Particularly in its inability to foresee how interest rate risk could cripple its fragile business model, which focused heavily on venture capital deposits. Venture capital tends to be flighty in periods of economic stress, so management could have easily assumed a drawdown in deposits would be forthcoming. The bank ballooned in deposits during the printing frenzy of 2020 - 2021. Customer deposits went from $61.76bn at the end of 2019 to over $189.2bn by the end of 2021! This was obviously unsustainable. As a professional money manager, what they did with the deposits is a real headscratcher. In an act of either pure laziness or pure speculation, the bank piled customer deposits into long-duration securities such as mortgage-backed securities or Treasuries without hedging the potential for a rise in rates. Recall that the longer the bond, the greater the interest risk. SVBs securities portfolio of $120bn had an average duration of 5.7 years. What this means is that for every 0.1% increase in rates, the bond portfolio would lose $700 million. Ask yourself, have you been in tune enough the past few years to assume rates would be moving higher?

Source: JP Morgan Guide to the Markets

The situation that ensued played out as predictably as the day is long. As companies drew down their deposits to meet ongoing cashflow demands (i.e. payroll), and venture funding wasn’t there to shore up account balances, SVB was forced to sell its long-duration assets in a rising rate environment to meet withdrawal needs. This put tremendous stress on the bank’s liquidity. Operations were not compromised until the bank sought Goldman Sachs’ advice to address potential liquidity concerns with an equity sale. When word got out about this, the stock plunged, and venture capitalists sounded the alarm with big names like Peter Theil advising account holders to withdrawal their funds. The rest is history. A good ole’ fashioned bank-run in the making, but this one only took two days.

What you probably didn’t realize, but you hopefully do now, is that your bank doesn’t keep your money on-site. In fact, less than 9% of dollars are circulated in physical form. The folks lined up at their local SVB branches probably didn’t get to withdrawal their money because the cash simply wasn’t there. FDIC, a government sponsored corporation that insures most bank deposits for up to $250,000, will cover smaller depositors. As a consumer, if you have more than $250,000 in a demand deposit account then you should go seek professional advice. SVB was unique in that 80% of deposits were over the insurable limit due to the nature of their business model, which partly explains why so many panicked. This motivated FDIC, the US Treasury and the Fed to issue a joint statement that they would do what is necessary to make all depositors whole. This statement covered not only SVB but all U.S. banks. While this event could have led to a wide-spread contagion fueled by consumer hysteria, fortunately cooler heads have thus far prevailed. Rest easy that your U.S. dollars backed by Federal fiat on deposit with your local bank are safe, for now. Let this be a reminder that there is no such thing as ‘risk-free’ in the world of money.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. Rebalancing a portfolio may cause investors to incur tax liabilities and/or transactions costs and does not assure a profit or protect against a loss. All investing involves risk including loss of principal. No strategy assures success of protects against loss.

Thank you for providing this information in a manner that less financially literate folks will understand.