Capital Pain Tax

Simple in concept, complex in application.

No pain, no gain. That’s what the meatheads say about life. Most health experts proclaim this statement to be fiction. Too bad. I would love to cash in on my lower back pain.

Fortunately, the inverse holds true for taxes. No gain, no (tax) pain. Capital gains tax is owed whenever you sell a capital asset for more than you acquired it for.

Notable exceptions to this include those held within tax qualified accounts, such as 401(k) plans or IRAs.

A short-term gain is realized when you sell for a profit less than 12 months from acquisition. All short-term gains are taxed like your paycheck, as ordinary income. Long-term is, you guessed it, a gain realized from a capital asset realized 12 months or later from acquisition.

Long-term capital gains tax is generally more favorable, so it pays to be patient.

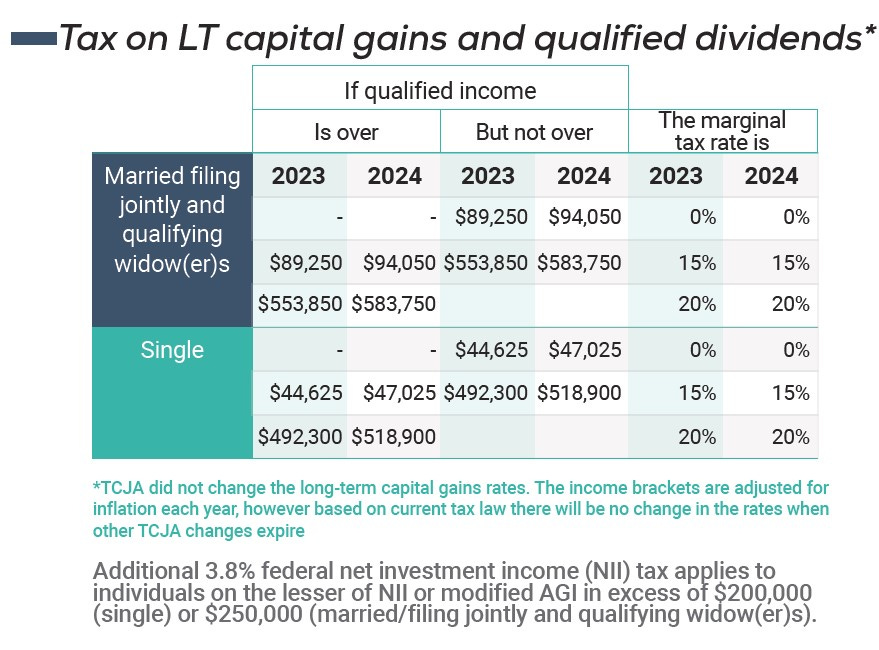

There are three long-term capital gains tax brackets. The rate you pay is determined by your taxable income, which accounts for your itemized or standard deduction(s). The more you make, the higher your rate. If you’re lucky, you make enough for the 3.8% kicker!

Deviations from the above chart include the tax on gains from the sale of collectibles at a fixed 28%, while unrecaptured section 1250 strait-line depreciation on sold investment properties is fixed at 25%.

Keep in mind, realized capital gains increases your taxable income, which makes it impossible to unwind a large sum in the lower brackets. Believe me, I’ve asked. The IRS was NOT nice.

There’s been a kerfuffle lately around capital gains tax proposals. It has become apparent to me that many do not understand this tax. Terms like “realized” and “unrealized” are thrown out with little explanation so let’s start from the ground floor.

A realized capital gain occurs when you cash in your winning investment, meaning you have materially transferred the capital asset for value. Most commonly, this means you sold the asset in exchange for cash.

Unrealized gain means the investment has a market value above your purchase price, but you have yet to ‘cash-in’, so to speak. Think of Jeff Bezos and his 912 million shares of Amazon. Or, closer to home, the appreciating house you continue to live in.

It is possible to offset gains with losses. Although, I would not advise seeking losses for this purpose. Someone should inform Cathie Wood.

Currently, capital gains tax only applies to realized gains. Usually, this coincides with receipt of cash, making it relatively easy to pay the tax obligation. It is possible to defer capital gains taxes indefinitely simply by using your appreciated assets as collateral for a loan in lieu of selling them.

“That’s the strat”, as my kids would say.

If you manage to defer this liability until death, your beneficiaries get a stepped-up cost basis. So, in a strange way, you can avoid one of life’s certainties, death, to avoid another certainty, taxes. See, dying isn’t so bad after all.

This is a strategy many wealthy Americans have employed for decades, yet now it has the attention of some policymakers. Why? Because it’s voting season. The outrage de jour takes aim directly at taxpayers with $100M or more in assets with an annual unrealized gain tax of 25%.

Taxing unrealized gains represents a significant departure from current policy. The spirit behind the recent proposal is to capture income tax on growth while in deferral for federal redistribution.

Problems quickly surface when analyzing its potential downstream effects. One of which would be a substantial reduction in the estate tax receipts, which could arguably negate the entire tax increase.

Forcing liquidations to pay the tax would not be conducive to properly functioning financial markets. The asset your employer may choose to liquidate could be your department. Talk about disruptive.

Furthermore, the policy would favor ‘old’ money wealth versus ‘new’ money wealth, further buttressing the class ceiling.

Like ink poured into a glass, tax policy meant to apply only to the rich likes to diffuse over time. Often, this is because congress defines “rich” without considering an inflation adjustment.

It will be interesting to watch policymakers squirm when their constituents begin paying capital gains taxes on home sales that exceed the primary residence exemption amounts set in 1997 ($250k for individuals, $500k for married).

The cost of the average home was $127k in 1997. Compare that to $450k today.

With the ratification of the 16th amendment in 1913, the Federal income tax only applied to Americans earning $500,000 or more. At the time, this was only 1% of the population. Boy, that sounds familiar.

It’s true. Capital gains taxes are taxes for the rich. What you may not realize is that you may, in fact, be rich. Definitions matter.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Individual tax and legal matters should be discussed with your tax or legal professional.

Securities offered through LPL Financial LLC. Member FINRA/SIPC. Advisory Services offered by National Wealth Management Group LLC, an SEC Registered Investment Advisory and separate entity from LPL Financial LLC.