Dropping Bombs

Major shifts in tariff policy while bombs fall over Iran

Our minds are inundated with news to such an extent that we have collectively become catatonic to actual bombs, both literal and figurative. For better and worse, Americans casually move about their lives whilst urgent notifications rattle in pockets and news broadcasters ramble about, serving as background noise for this evening’s dinner prep.

Buzz words no longer vibrate our consciousness like they used to. In an endurance race against narrative, spectacular imagery is measured by dubious eyes scanning for telltale signs of AI interference.

The American mind stews in a pot of acidic broth served up to hungry data farms. The economy of attention may be smothering itself.

The past two weeks we learned, as I predicted, that the Trump Administration’s use of the International Emergency Economic Powers Act (IEEPA) was unconstitutional. One short week later on a Saturday morning, we also woke up to news that U.S. and Israeli war planes penetrated Iranian airspace with unprecedented force, destroying key IRGC targets with frightening veracity.

The only thing more surprising than the aptly named Operation Epic Fury is the fact that I received zero calls to discuss either topic the following Monday. Whether it be apathy or maturing investment behavior, most of America responded to the news with little concern.

The most likely explanation is as old as the theme of ‘The Boy Who Cried Wolf’. The sentiment of our culture can be wrapped up in one simple memetic: nothing ever happens. Major things happen all the time, we just began discounting their significance because

A) we don’t know what to do about them, or

B) we can’t afford to do anything about them

The lingering question remains: is there actually a wolf hidden over the horizon and what should be done if so?

These are both major events that will have long-term socio-economic consequences. Like wolves in the distance, their presence does not determine fate, but they should be respected, acknowledged and factored into your investment plans.

Tarifs

Money Alchemist EP 51 | What’s Next for U.S. Tariff Policy

In a 6 - 3 decision The Supreme Court effectively took away the President’s scariest looking stick and threw it into the burn pile. The remaining options, twigs by comparison, remove the Chief Executive’s ability to unilaterally, and unpredictably, negotiate tariffs on an indefinite basis.

In other words, President Trump’s wild-card approach to trade negotiations is now off the table. This explains how the White House can hold two contradicting positions at the same time:

A) Using the IEEPA as the first-choice option for tariff policy, and

B) Suggesting the alternative options provide an improved framework for tariff implementation that could result in MORE tariffs

Let’s talk about those alternative options.

Section 122 - Trade Act of 1974 gives “balance of payments” authority for 15% tariffs for 150 days - requires Congress to extend. This is what’s being used to bridge the gap until Section 301 or Section 232 tariff policies can be implemented.

Section 301 - Trade Act of 1974 - Expanded via Omnibus Trade and Competitiveness Act of 1988 - Office of the US Trade Representative must investigate and determine unfair trade practice which could result in tariffs to balance trade.

Section 232 of the Trade Expansion Act of 1962 - Department of Commerce Bureau of Industry and Security - investigation must uncover risk to national security - tariffs can be used as retaliation measure if a threat is determined.

Both Section 301 and Section 232 tariffs take time to implement (60 – 180 days), requiring comprehensive coordinated investigations and telegraphed implementation. They cannot be changed on a whim and do not fit nicely into an aggressive real-time negotiating tactic.

This is bad news for the Trump Administration, which relies on shock and awe muscle flexing to progress its America First agenda, aiming to boost domestic manufacturing. While the plan is to move forward with the limited tool set, this is a decisive win for globalization.

What this means for you:

Lower tax-drag on cost of goods sold (i.e. potentially lower prices)

Favors global corporate profits

Reduced potential market volatility due to tariff shocks

Lower incentives to reshore could soften U.S. jobs growth

Iran

We’ve been hearing for more decades that Iran is on the verge of attaining a nuclear weapon. While a legitimate ongoing fear, eliminating Iran’s nuclear capabilities feels more like a plausible cover for the extreme measures taken than a primary mission objective.

More likely, the opaque objectives are the calculated result of a complex set of datapoints synthesized by an advanced wargames apparatus. Pentagon doctrine integrates the most advanced artificial intelligence systems money can buy into operational planning, courtesy of $1 Trillion of your tax dollars (the 2026 US Defense budget).

(I wonder how they came to define “intelligence” this way? 🤔)

Many, who are not ‘read in’ at the prerequisite TS clearance levels, espouse their highly inflated 2 cents on the evolving situation. I am no such person and offer only speculation and my predictions for economic consequence.

Though many are disheartened that yet more military involvement has been deemed necessary in the Middle East, it appears to be motivated by opportunistic geostrategic realignment and alliance incentives rather than pure defensive necessity.

Remember that just one month prior, Nicolás Maduro was ‘extradited’ by U.S. special forces in Operation Absolute Resolve. Venezuela happens to be a major U.S. oil exporter as with Iran. Approximately 20% of the world’s oil passes through the Strait of Hormuz, largely controlled by what was the Iranian Navy now diminished to small fishing boats operating drones.

The flow of this oil disproportionately benefits China, much of it trading outside of the US dollar. A theme emerges…

We do not know to what extent the conflict will be contained to the region, whether the mission objectives will be achieved or how China will react to the event. But the odds are high that all these risks were ‘intelligently’ measured prior to the strikes, and more than one person acknowledged the light was green.

What it means for you:

Temporarily higher oil-based product prices – likely through the summer

Stronger dollar – headwind for unhedged international positions, but good for U.S. imports

Heightened readiness status for active military families

Supports longer-term oil price stability and dollar hegemony

Globally increased defense spending

Bottom Line

Both headline events impact markets in different ways with a few clear takeaways.

The U.S. dollar, thus far, has strengthened in response to the events which tracks with logic. If continued, this should help moderate domestic inflation on imported goods.

International stocks have sold off sharply with the iShares MSCI Total International Stock Fund down -7.3% since its February 25th all-time-high. This could present a good opportunity for investors looking to add international exposure who may have missed the earlier run.

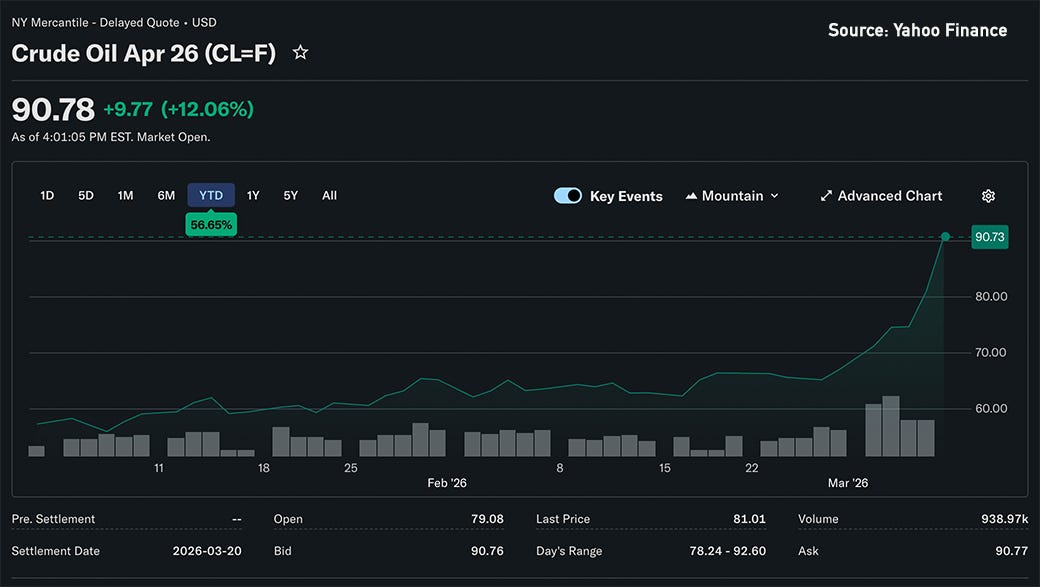

Oil, the most affected commodity and the bedrock of the modern economy, is the obvious concern. April 26 crude futures trading on the NY Mercantile have risen sharply and are up +56.5% year-to-date at over $90 per barrel.

A reasonable expectation is for this to be a temporary situation and should be ignored by long-term investors disinterested in speculative trading. Otherwise, now may not be a bad time to buy gasoline futures for your July 4th road trip.

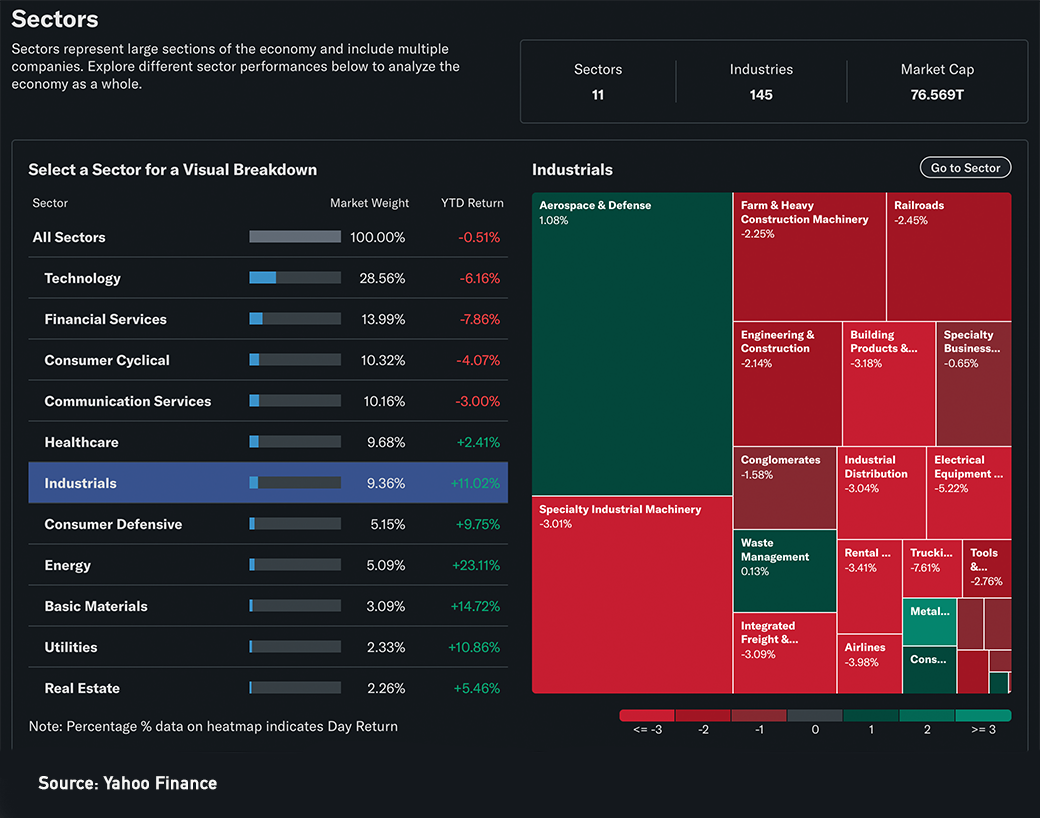

The industrials component of the S&P 500, dominated by Aerospace & Defense, are up +11.02% so far in 2026. Given the state of current global affairs, industrials look particularly compelling to investors.

Modest adjustments to a diversified portfolio should be considered in light of recent developments, but not much more. Undiversified (i.e. concentrated) investments should be reviewed with discernment. Diversification becomes even more important as uncertainty mounts.

It might be a good time to shake off that feeling of apathy and consult with a financial professional. There’s a lot to unpack here.

Investment advice offered through National Wealth Management Group, LLC, a Registered Investment Advisor.

The information presented is for educational and informational purposes only and is not intended as a recommendation or specific advice. Investing involves risk, including the potential loss of principal. Past performance is no guarantee of future results.

Please consult with a qualified financial, tax, or legal advisor before making any decisions based on this information.