Electric Boogie | v2026

The dance to new highs continues despite popular sentiment

Something is wrong.

Feels have never been so low and stock prices never so high. The disconnect between sentiment and asset prices is so wide that Evel Knievel wouldn’t attempt to jump it.

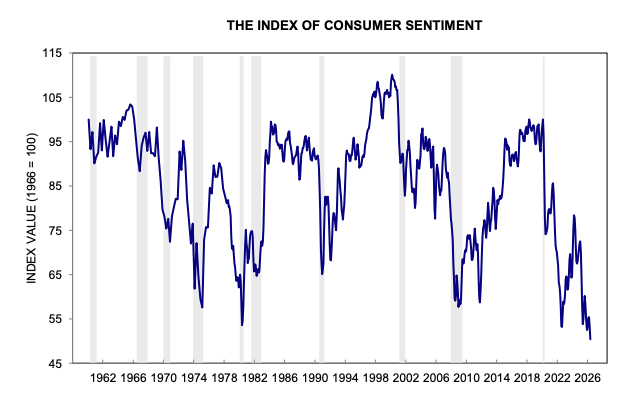

The Michigan Index of Consumer Sentiment is lower than it has been in the past 50 years.

Lower than the oil embargo of the 70s.

Lower than 9/11.

Lower than the Great Financial Crisis.

Lower than the lows of the COVID-19 era.

Yet stock most stock indexes, including the S&P 500 and NASDAQ are kissing new highs more regularly than a mother her newborn baby. It’s so frequent that onlookers are now concerned about contagion.

Perhaps this is driving sentiment, but I think not. In 2024, the Michigan Index of Consumer Sentiment shifted from gathering data by telephone to web-based surveys solicited by mailers with a QR code. It’s sent out to 900 – 1,000 participants, excluding Hawaii and Alaska residents (their opinions don’t count, presumably due to too little or too much sunshine exposure).

Shifting from phone to mail responses was necessary as Americans reacted to the scam-call epidemic. Unfortunately, it also adds friction. Now respondents have to open the mail, scan the code, wait for the survey to load, then submit responses.

Who’s more likely to bother? The person with a complaint, or the one who’s perfectly content? If you’re unsure, just ask the manager at your favorite retailer then prepare for a trauma dump that will test your faith in humanity.

Negativity bias is hardwired. An infant cries much louder than it laughs.

The University of Michigan does what it can to counteract this bias, such as using neutral wording and random sampling, but the shift from a quick unsolicited phone call to mailed homework is going to skew results.

Layer on a politically polarized populace, many of which are ideologically discontent, and we can approximate a logical explanation. Mystery solved.

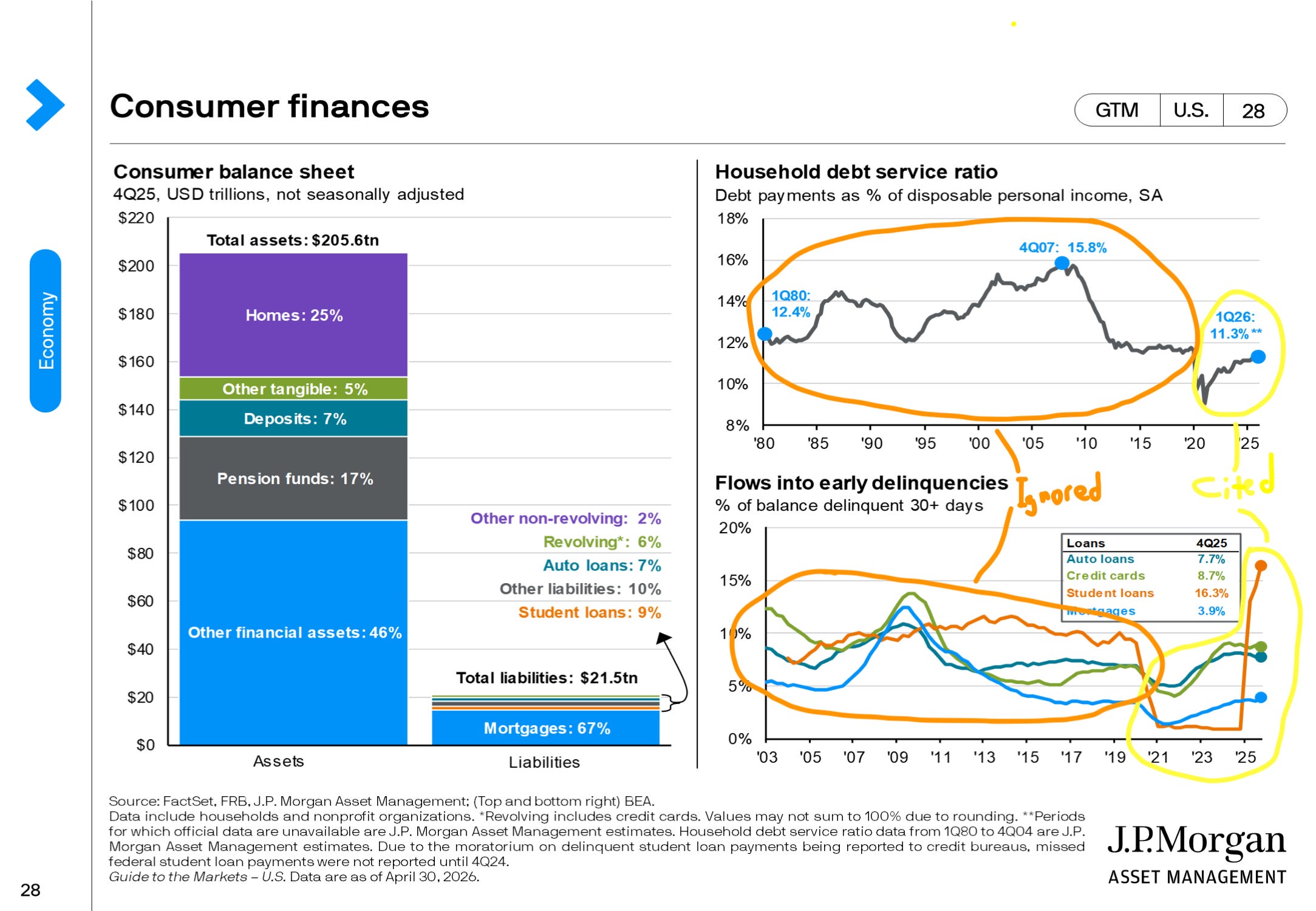

But how do we excuse the news around record level loan defaults, the housing affordability ‘crisis’, and the general plight of the bottom 50%? Truth isn’t so easy to find when it is painted over with statistics.

Every chart should be viewed as if it were a crime scene. Always read the footnotes and question the reliability of the source data. Anyone with a modicum of talent can make a chart sing their favorite song with a little orchestration.

Take, for example, the notion that loan defaults are at ‘peak’ levels. Yes, since 2021 but not hardly since before that. Adding color such as “debt at levels before never seen” is equally misleading given the reality of inflation, but carries an effect, nonetheless.

The housing affordability crisis is not ‘crisis’, but a reality check. The 2010 – 2021 period gave us subsidized mortgage rates, courtesy of Quantitative Easing, and a market still whiplashed by the GFC. It was the golden era for new home buyers!

The return to normal, albeit with some overcorrection exacerbated by the COVID stimulus response, feels like punishment. Recency bias tilts our opinions to favor the theory that housing is overheated. Yet homes continue to sell at higher prices, defying buyers pining for prices from the past decade.

And as for the bottom 50%, yes, they struggle. But tell me something new. Dave Ramsey built a multi-million-dollar empire preaching to this segment on the virtues of sound money management. Business has been booming since the early 90s.

The statistic that “60% of Americans live paycheck to paycheck” has been consistent for decades. It might even be an economic principal. Now there’s a dissertation idea for some aspiring finance graduate student!

This is not to dismiss the genuine struggles experienced by this cohort, but simply to explain that their mere existence should not permit us to believe the doom and gloom narratives without context. Things are just not as bad as they are portrayed to be.

Financial markets are telling us economic conditions remain quite good. Many people can’t, or won’t believe it, so they cling to a counter-narrative that confirms their priors. Emotional anchors sink deep into personal fiction, and suddenly we forget the laws of physics.

Sorry to break it to you: markets don’t care about your opinions any more than gravity does.

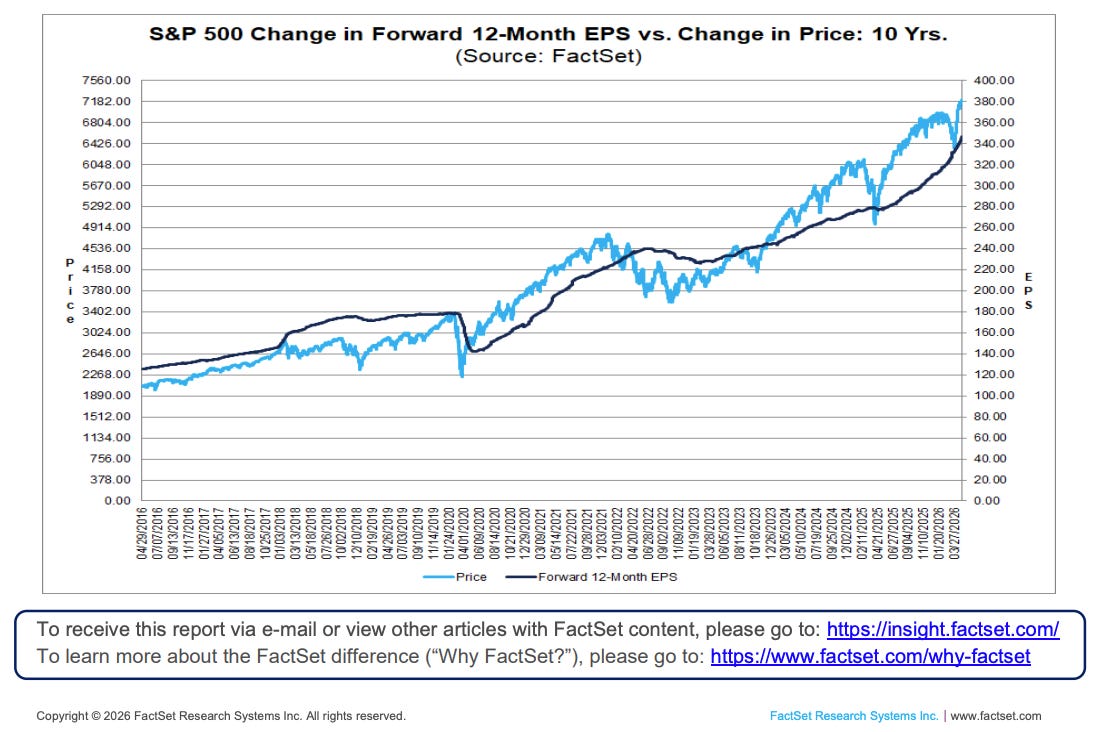

The S&P 500, Nasdaq, and most global indexes have marched to new highs in 2026 for one primary reason: earnings. The more money a company makes, the more it should be worth. Simple logic like this beats opinion over time.

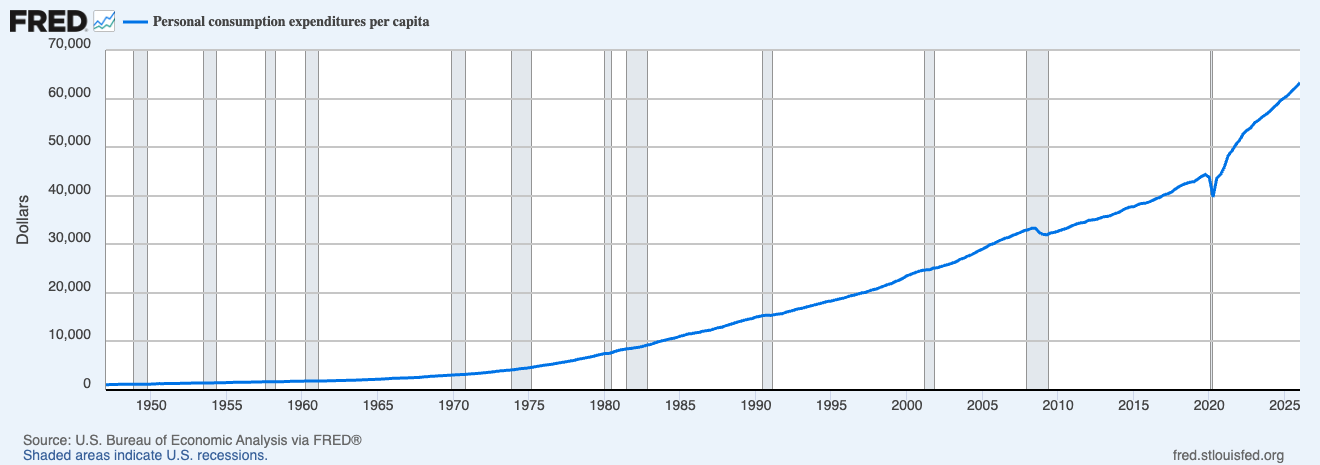

There is more than one singular force driving recent results, but the most influential one is you. Consumption is at or near all-time highs. We simply cannot stop going to Costco. It has to be the cinnamon rolls.

But there are other factors as well:

Massive infrastructure investment to support the AI revolution (i.e. “picks & shovels”)

Strong projected government spending, especially defense, and

Stimulative tax policies

When we clear our heads of the social media malaise and look around the restaurant table we waited twenty minutes for, we should ask ourselves:

“Does this feel like a bear market?”

Whether or not we pay the final bill with the last dollars in our checking account doesn’t matter. Around 2/3rds of the patrons, statistically speaking, have always been doing that. So long as they’re employed the party continues.

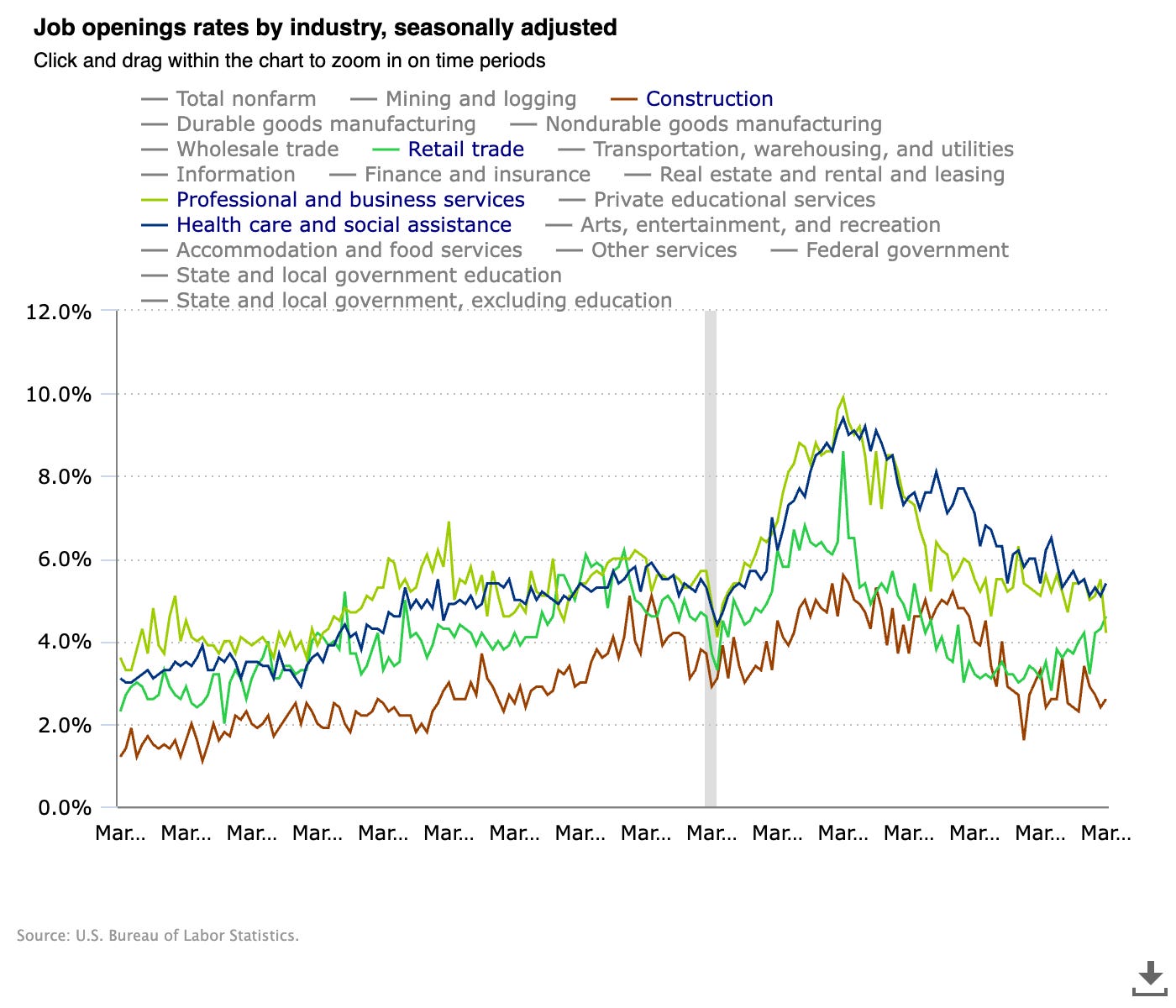

Which brings me to the final segment of this week’s long-winded rant: jobs. It’s all about the jobs. And here things seem rather…normal.

No AI jobs apocalypse. Another boogieman.

Tell me exactly how Claude is going to lay the foundations for next-gen data centers generating responses to your growing number of inquiries? How is Gemini going to run the miles and miles of copper required to power its own hardware? And how is Grok going to mine the copper?

Unprecedented levels of electricity demand alone could supply our future economy with more than enough jobs to offset layoffs caused by labor displacing AI agents. Your AI inquiries will always terminate with some form of human action.

Humans are the beneficiaries.

Technological advancements do not create economic recessions. Human behavior causes recessions. Policy errors, baseless speculation, energy shocks, pandemics, and wars – these are the economic hitmen.

While these hitmen are ever-present, they seem to be too busy dancing the Electric Slide to derail equity markets at the moment. Sometimes the music is so compelling that even party poopers join the fun.

Investors should stay the course. New homebuyers should buy the house (with responsible degrees of leverage, of course). And we all need to stop trying to time our exits the precise moment the music ends.

There’s always another song to be played.

Investment advice offered through National Wealth Management Group, LLC. The information presented in this newsletter is for educational and informational purposes only and is not intended as a recommendation, solicitation, or specific investment advice for any individual.

The S&P 500 and NASDAQ Composite are unmanaged benchmarks designed to represent broad U.S. equity market performance and cannot be invested in directly. Past performance of any index, security, or strategy is not indicative of future results.

All data, charts, statistics, economic indicators, and survey results (including the University of Michigan Index of Consumer Sentiment) referenced herein are obtained from sources believed to be reliable; however, their accuracy, completeness, and timeliness cannot be guaranteed. Economic and market data are subject to revision without notice, and charts are presented for illustrative purposes only.

The opinions expressed are those of Benjamin Jones as of the date of publication and are subject to change without notice. They do not necessarily reflect the views of National Wealth Management Group, LLC. Readers should consult with a qualified financial advisor, tax professional, or attorney regarding their specific investment objectives, risk tolerance, and financial situation before making any investment decisions.