Fee Fi Fo Sum

The intimidating process of shopping advisors

Few professionals think more highly of themselves than financial advisors.

“Changing peoples’ lives”, they whisper to one another as fee schedules for the coming year are adjusted for ‘inflation’. This systemic pride is a consequence of a brutally discerning consumer who favors confidence over accuracy.

The application of Darwin’s law favors the self-assured individual, often harboring an ego with its own gravitational pull. Some of the most charismatic people I’ve met are in the money business, a powerful force in a delicate profession.

There are even hierarchies of purity within the advice circles. At the top, the self-proclaimed ‘paragons of objective advice’, are the fee-only advisors. They joust around the tiltyard armed with circular arguments, debating the perfect business model that removes all conflicts of interest.

The debate is interminable because the core conflict can never be eliminated:

An advisor is hired to increase his clients’ wealth but is simultaneously compensated directly from this very wealth.

The debate rages ever onward. Consumer would be amused if they were aware.

And at the bottom we have the lowly life insurance brokers. Universally disliked in all financial planning circles, they serve dutifully as punching bags for the alpha professionals requiring superiority bias confirmation. Whether the anathematic reputation is deserved is truly subjective, but secretly, the fiduciaries are glad they exist.

It is entertaining to disconnect from this industry and surveil it from afar, from the perspective of someone that has no dog in the fight. This examination helps me ground my own ego but also forces me to address the question of whether I would hire a financial advisor knowing what I know.

Truthfully, it’s not an easy question to answer.

Like the sausage industry, consumption of product becomes more challenging the more that is known. The process itself is less frightening than the awareness of how easily nasty bits get thrown in without the end consumer knowing it.

I’ve read the disclosure documents. While I legally must tell you that these are important documents that inform your decisions – technically true – I also know that they provide as much epistemic value as C-SPAN. Real people operate mostly on trust, not disclosure text. In fact, the more disclosure text, the lower the trust.

Trust is either earned directly (rare) or it is outsourced through a friend or some other resource like online reviews or videos, which is not very reliable. Most people are overconfident in their ability to judge character, and online reviews are largely curated these days.

To add to the problem, recall that successful financial advisors have been naturally selected for their confidence. You see the issue here. It’s like accidentally acknowledging the AT&T salesman at Costco thinking you can just perform a friendly walk by.

It may be better to sidestep the whole minefield and avoid hiring an advisor altogether, an attractive option based on surface level issues. It is very possible that an AI + DIY method is the way to go. Let’s ask ourselves,

Does your spouse know what you know or more about your money situation?

Do you understand what your investments are and how they work for your situation?

Do you know how much you should be investing and where?

Do you usually accomplish money related goals you set for yourself?

Do you know everything you should be doing now to secure your future?

Are you familiar with your tax situation and how it impacts your investment plan?

A ‘no’ to any one of them may mean an advisor can add value, which also means the lazy route is no bueno. Personally, I can answer ‘yes’ to all but the first one, which makes this a question of how much I love my wife.

As it turns out, enough to hire a financial advisor. A good one at least, preferably with a slight overconfidence bias. While my situation is a bit different given my own designated advisor doubles as my succession plan, anyone can apply the method I used to qualify this person.

Value for Fee

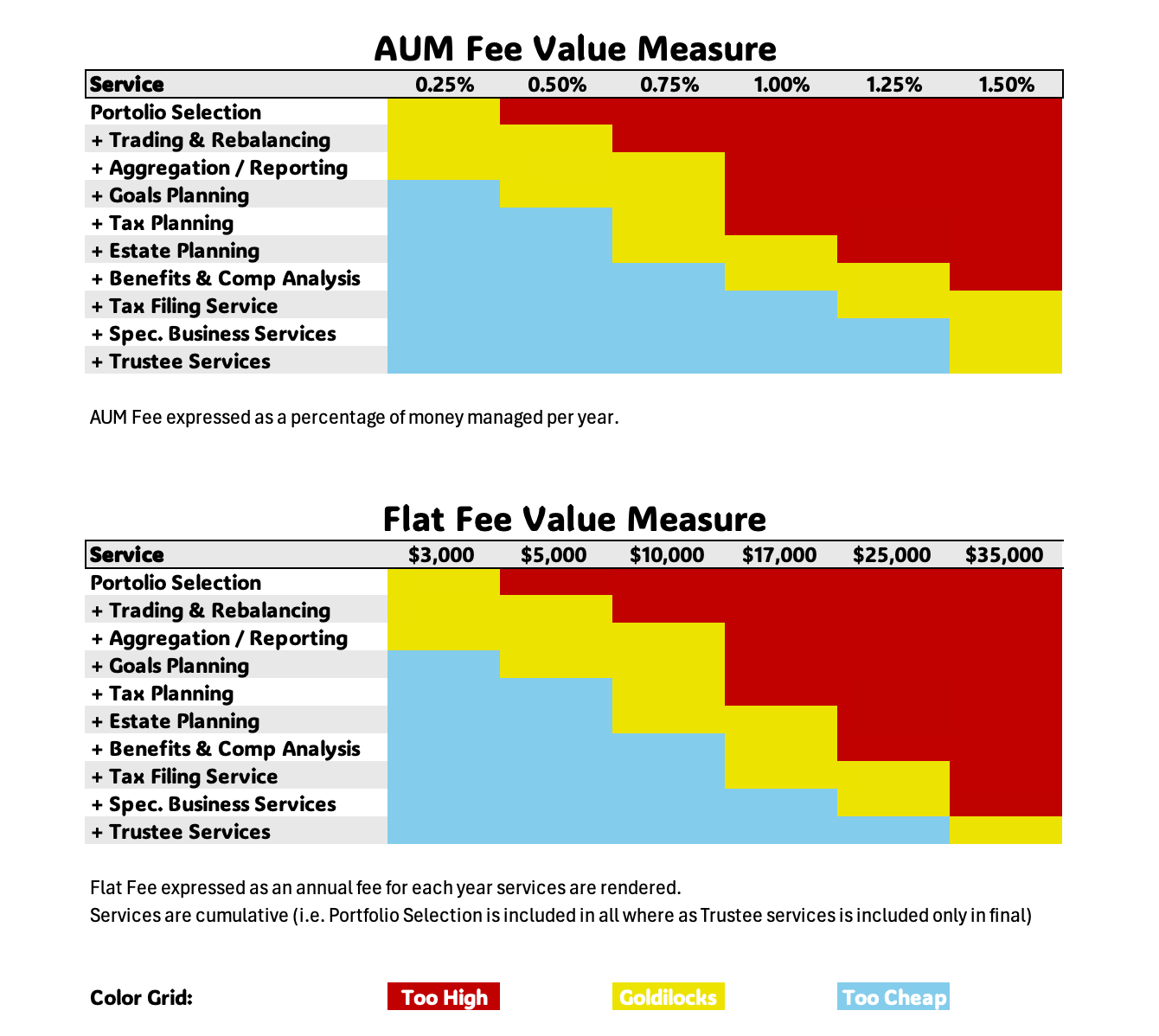

The prima facie assessment every person naturally makes is cost. And for good reason, it’s literally money out of your pocket. Consumers are accustomed to intuitive pricing with standardized goods and services. A Pepsi is roughly equal to a Coke, but this is not the case with financial services.

Not all firms are equal even if the fees are. Some advisors won’t even look at your 401(k) plan for fear that it might assign them unwanted liability. Attempting to standardize the most common services in a progressive order, I put together two charts to help us map value for cost.

The way to read the charts is to look at the fee in the X axis and match it with the cumulative service list in the Y axis (each service is a natural add-on from the one above). The two charts are meant to be independent from one another, representing its own fee structure.

If the box is red, that means the fee is too high relative to the cumulative services being offered. Suspiciously cheap is also problematic and could imply a less informed service. The sweet spot is the Goldilocks zone.

Value is subjective, but this is where I draw the line for my household. The higher the fee, the more that needs to be offered. Simple, really.

Personal Judgment

Now that we have that formality out of the way, I want to propose seven unconventional but very real questions you should ask when shopping financial professionals.

Imagine this person with a bullhorn, would you suffer hearing loss by the end of the meeting?

Would you allow this person to watch your pet over the weekend?

Does their office space look like it was furnished by Goodwill? Do they even have an office?

Did you feel compelled to terminate conversation at any point out of boredom or discomfort? Whether you acted on this compulsion doesn’t matter.

Are they competent enough to publish their methodology online and, if not, why the secrecy?

If this person was your college finance professor, how often would you skip class?

Does this person motivate you and improve your outlook on life?

These questions could reassure your gut-check, something that should not be ignored. A perfect score isn’t required but anything short of five favorable responses is a swipe left in my app.

Lastly, Standard of Care

The f-word gets thrown around a lot, so much so that its meaning has lost potency. A fiduciary standard of care is the highest available and should be the only choice for investors who want their advisors to put their money where their mouth is.

This entails working with a fee-only advisor. It’s possible to work with a fiduciary that also earns commissions in certain capacities, known as fee-based, so it’s important to ask when and where the fiduciary standard applies. Generally, it will be detailed in an advisory agreement signed by both client and advisor.

The following ‘financial advisors’ are not fiduciaries:

Subscription newsletter authors (sorry readers, you need to hire me first)

Brokers (i.e. insurance, mutual fund, stocks sold on commission)

Bolt-on free planners provided by your employer plan

Financial entertainers consumed via video or podcast

Advice from friends

Generally, if you are not explicitly paying a pre-defined fee clearly deducted from an account you control, you are not working with a fiduciary. There are exceptions to this, but they are rare.

The battle for pinnacle purity among fee-only advisors may never end, but they rightfully wage war at the top of the hierarchy of the Advice industry. Consumers can only benefit from this competition and it’s the only place I would shop for a financial advisor.

Sorry brokers, but there’s nothing stopping you from joining those ranks. Time to step up.

So, I conclude my disembodied review of the industry I call home reassured that my self-confidence in what we do is not misplaced. Yes, financial advisors tend to think highly of themselves, but a good one deserves to. Hopefully this article will help you find them.

Investment advice offered through National Wealth Management Group, LLC.

The information presented is for educational and informational purposes only and is not intended as a recommendation or specific advice. Past performance is no guarantee of future results.

Consulting with a qualified financial advisor who understands your unique situation is recommended before making any investment decisions. Fee structures, fiduciary standards, and services vary by advisor and firm. Always review agreements carefully.