Top 3 Social Security Mistakes

An Insider's View

Rather listen?

Check out our latest episode of The Money Alchemist Podcast with guest Social Security veteran, Jim Blair! Available on Spotify, Apple Podcast or wherever you get your podcasts.

Ah, Social Security, everyone’s favorite government program to hate on but can’t live without. Established in 1935, the Social Security Act was passed in response to an epidemic of elderly citizens living below the poverty line. Today, more than 40% of retired Americans count on Social Security as their only source of stable income.

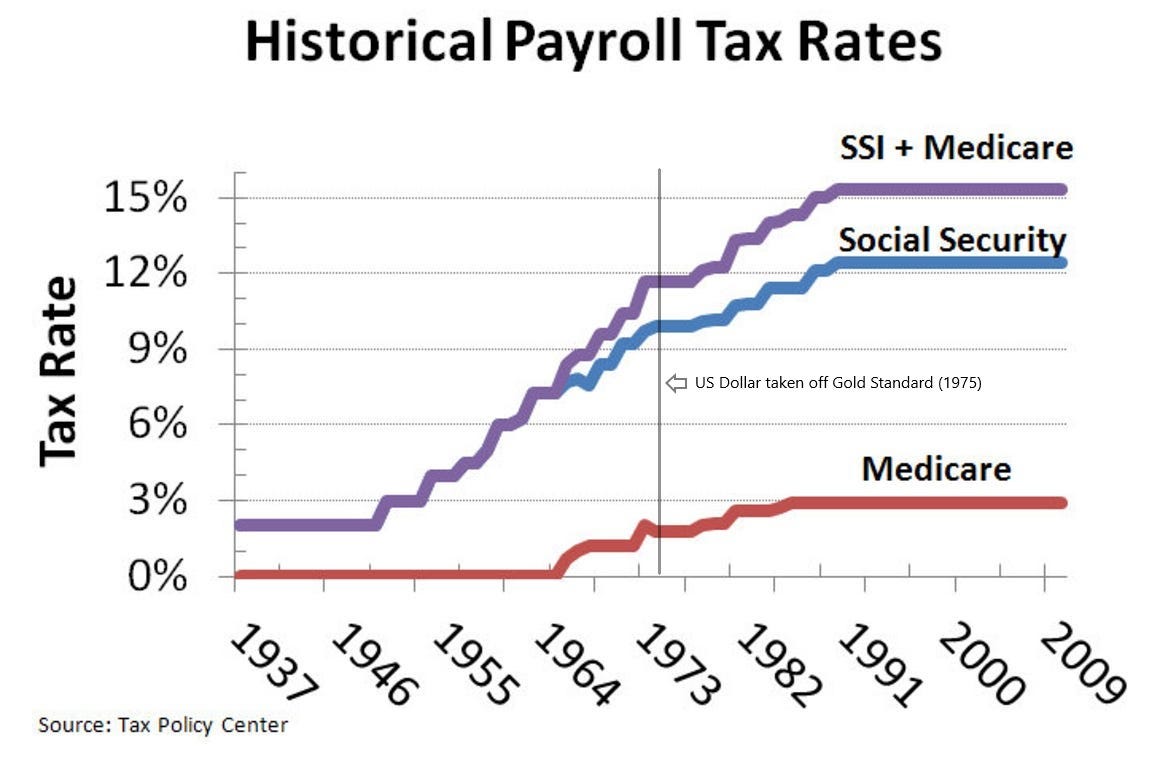

While living just off Social Security wouldn’t put you in a position full of options, you can at least afford to opt out of the Fancy Feast meal plan. Need it or not, it’s smart to optimize your benefits. You pay for them, after all. 6.2% of your compensation up to $168,600 in income in 2024. Your employer matches this amount for a total tax of 12.4%, just for Social Security alone.

As the Italians say, that is a spicey meatball. But it’s the meatball that sustains retired America and it is not going away. Regardless of what the sensationalists in the media say. It is true that the OASI Trust will exhaust its surplus by 2035, IF nothing changes. The key word is upper case for a reason.

Things will most definitely change.

Furthermore, IF nothing changes this does not mean benefits vanish. They would simply be reduced to equal the income tax revenues dedicated to the program. Estimates put this reduction in benefits at 28%.

The program is not permitted to run at a deficit. Yet. We know how our policy makers love deficits. Now that a think about it, opening an exorbitantly priced steakhouse in DC under the name The Deficit would be a banger hit.

But that’s not the subject I want to focus on today. It’s a concern for the next decade, for sure, but it doesn’t change today’s priorities. These should include avoiding the three biggest mistakes people make when dealing with Social Security. At least according to the opinion of Social Security veteran Jim Blair with Premier Social Security Consulting.

I recently had Jim on our podcast this past week and we talked about all things Social Security. For the bullet points only crowd, here are some take aways:

Mistake 1: filing for your benefit without considering your spouse.

Let’s face it, life is not like the Notebook. One of you is going to die before the other and that means one of the Social Security benefits is going to terminate. When deciding whether to file later for a larger benefit, consider that this larger benefit will last for two lives and not just one. The surviving spouse should be able to keep the higher of the two benefits.

Mistake 2: filing at age 62 if income isn’t needed.

Social Security is not going away any sooner than politicians turn away votes. Also, don’t kid yourself by thinking you’ll just invest your Social Security benefits to outpace inflation. This simply does not happen. The early retirement benefit is reduced by $1 for every $2 in earnings over $22,320. If you’re lucky enough to have enough phantom income to draw an unreduced benefit, you would still need to maintain savings discipline. I can count the number of times I’ve seen this work on my third hand.

Mistake 3: counting on the Social Security Administration to catch mistakes.

As Jim mentioned in the podcast, the Social Security Administration is full of highly capable people, and they are there to help you get what you qualify for but not necessarily to consult. Mistakes happen and it’s impossible for the SSA to debug every error within the millions of records they maintain. It is up to you to know what you qualify for and to update your information as necessary. Jim recommends everyone over age 18 set up an SSA.gov account and regularly (once per year) review their records. Working with a qualified Social Security advisor is also a good idea as you approach important filing decisions.

If you are reading this article and maintain US citizenship, Social Security will be a part of your retirement plan. The program will certainly change to maintain viability, so your retirement plan should also be flexible.

The more retirement savings you have, the more flexibility your plan has. The earlier you start getting serious about saving, the larger your portfolio by Full Retirement Age (FRA). I know it can be challenging to prioritize some ambiguous future date over the here and now. Decisions, decisions.

But, if you spike the ball and fail to save enough to make you comfortable, you should still have Social Security. The question isn’t whether the program will be there, it’s how much your benefit will buy. If history and political incentives are anything to go by, reform is likely to involve an unhealthy dose of deficit spending. And you know what that means: money printer go “burrrrr”.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Securities offered through LPL Financial, member FINRA/SIPC. Investment advice offered through National Wealth Management Group, LLC, a registered investment advisor and separate entity from LPL Financial.