Usury is the Law

Charging interest is in your interest.

Sometimes, new information hits you like one of Mike Tyson’s legendary hooks to the body. Lightning fast, merciless, painful but unforgettable. The IRS is a lot like Tyson. You don’t mind watching others get wrecked from a distance and even admire the tenacity.

Rumor is, Mike is a touchy person. You don’t want to say or do anything that can be misconstrued as an invitation to the ring.

That is unless you are a bold fighter with more pride than survival instinct. Most of us make honest attempts to play by the rules to avoid a lopsided fight. Rules that happen to be more confusing than a game of Dungeons and Dragons with a schizophrenic dungeon master.

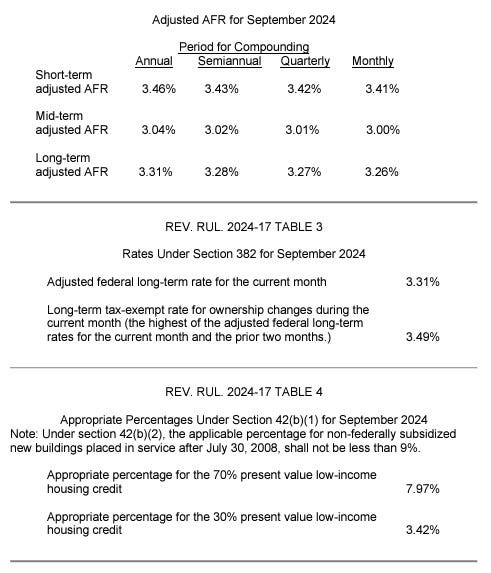

One such rule involves imputed interest. This is a payment deemed to be made by a borrower to a lender when the interest rate on the loan is less than the applicable federal rate (AFR). What is the AFR, you might ask? Have fun deciphering the IRS publication below:

Like a reasonable person, you may think this only applies to institutions in the business of lending. Ah, but that’s where you’re wrong. Enjoy the punch to the kidney as the IRS reviews your 1040.

The most common situations where imputed interest is applicable are in private lending arrangements. Let’s say you have kind parents, and they really want to see you buy that house that’s not too far but not in the same neighborhood. It just so happens to be out of your price range.

They may think, “Let’s just give them the money and they can pay us back the principal. Even Stevens”. Let’s set aside the questionable wisdom of ‘lending’ money to friends and family for a minute and look at what the IRS thinks of this arrangement.

As the tax code is currently written, this is considered an exchange of value. And you know what the IRS thinks of exchanges of value. Cha-ching. If your own mother lends you money without interest with the expectation of being paid back, she will need to report phantom interest (imputed interest) on the principal balance outstanding each year equal to the AFR.

Let’s say the amount is $100,000 and the AFR is 5%, the amount of taxable phantom income your mother would need to report is $5,000. It gets even more complicated because we also need to consider the borrower’s potential liability.

It could be considered a taxable gift if the amount of imputed interest is over the $18,000 annual gift-tax exclusion. It could be considered taxable income if the lender is an employer or business.

There are de minimus exceptions that exclude amounts of $10,000 or less. However, any amounts greater than this are subject to the reporting rule, details for which are beyond the scope of this article.

So, if you were thinking of lending or borrowing money privately, it might not be as private as you think. A good CPA or tax advisor might be able to help iron out the details.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Individual tax and legal matters should be discussed with your tax or legal professional.

Securities offered through LPL Financial LLC. Member FINRA/SIPC. Advisory Services offered by National Wealth Management Group LLC, an SEC Registered Investment Advisory and separate entity from LPL Financial LLC.