HSA – The Financial Health Supplement

Describing the Health Savings Account

Spending money on healthcare is like buying tires for your car. It’s woefully lacking in entertainment value and annoyingly expensive. Unless you want your health to careen off a cliff like a car in a rainstorm with bald tires, you should embrace the monetary bloodletting.

But most people love fun. This is why the standard American way is to scramble for comprehensive health coverage while malignantly neglecting self-care. We cannot reasonably expect any slowing of healthcare cost inflation until this behavior changes. Who knows if it ever will.

As a consumer of healthcare, your situation is not hopeless and there are many things you can do to reduce the risk of catastrophic health expenses. Granted there are many situations in which nothing can be done. Regardless, every health problem is easier to tackle by taking better care of yourself and your savings.

I’ll stick to what I know and focus on the financial aspect of health-maintenance.

MySpace launched in 2003, unleashing a virus that has since evolved into the societal affliction we now call social media. The universe attempted to balance this misfortune with the passage of The Medicare Act, creating the Health Savings Account. Not a fair trade, but it’s something.

In response to surging healthcare premium costs, many companies began to offer more affordable High-Deductible Healthcare plans (HDHP) as an alternative to the higher-cost co-pay policies. The idea was to shift the maintenance costs back to the insured to limit overuse and moral hazard.

The HSA was intended to encourage people to adopt HDHP policies. Congress envisioned the account as an add-on benefit employers could offer to compensate for the higher deductibles. People are generally hesitant to spend down personal savings, so it was reasonable to expect this could cool premium inflation by decreasing policy utilization.

But we’ll never know for sure because the Affordable Care Act was passed a short time later, shifting the entire health insurance paradigm. Fortunately, like the shrew post Chicxulub impact, the HSA survived the sweeping omnibus legislation.

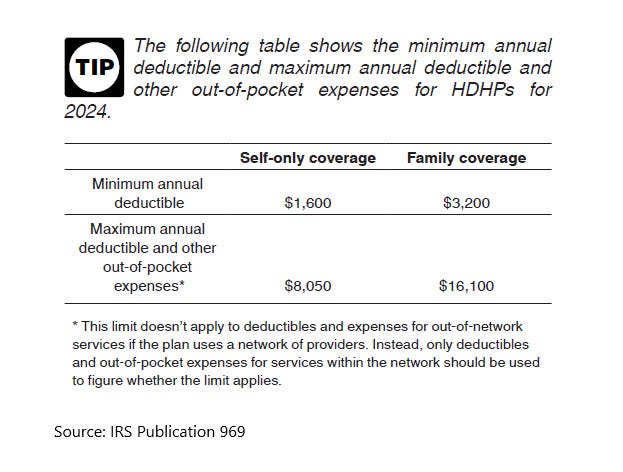

Today, anyone covered by a high-deductible healthcare plan (HDHP) can contribute up to $4,150 into an HSA for 2024.

Families covered by a HDHP can contribute $8,300 for 2024. The HSA does not work like an IRA, however. The family contribution can be made to a single account instead of two separate accounts under two different tax IDs.

The differences do not end there. Catch-up contributions begin 5 years later than IRAs at 55 and terminate at age 64. There are no early distribution penalties from an HSA unless the funds are used for non-qualified expenses.

Once the account owner is age 65, the balance can be used for any purpose to avoid the 20% excise tax penalty, however ordinary income tax for non-qualified expenses still applies.

“What’s a qualified expense?”, you may ask. In classic IRS form, the answer can be found by reading not one, but two IRS publications (Publication 969 and Publication 502). Too complicated? Perhaps we’re just not sophisticated enough to understand.

A best-effort summary of “qualified” expenses as per IRS Publication 502 is in the foot notes for those interested. As always, consult with your tax professional for an authoritative list or reference the IRS publications. 1

The most interesting, dare I say exciting, thing about HSAs is that they are triple tax advantaged. Contributions are tax deductible, earnings are tax differed, and distributions are tax-free for qualified expenses. There are no income limits placed on the use of HSAs.

The government has given us a tantalizing taste of what it was like to save money before income tax laws existed. It drives the Libertarians crazy!

Jokes aside, this is a pretty big deal. Many financial planners estimate around $250,000 will be spent on healthcare throughout the average retirement, so any opportunity to optimize lifetime taxation is helpful.

People between 55 and 64 can contribute an extra $1,000 per year as a catch-up contribution. For the ultimate HSA catch-up contribution hack, separate your family contribution into two different individual HSAs and you’ll get the $1,000 catch-up on both accounts!

Then there’s the matter of custodial options. Most simply default to the financial institution selected by their employer, which is generally the most convenient. Just keep in mind that not all custodians are equal, and you have a choice. What’s right for you depends on your circumstances.

Things to consider are the costs, investment options, ease of administration and access.

Any specific recommendation goes beyond the scope of this newsletter. I have an opinion, but it may not be the right one for everyone. That’s all for now.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Individual tax and legal matters should be discussed with your tax or legal professional.

Securities offered through LPL Financial LLC. Member FINRA/SIPC. Advisory Services offered by National Wealth Management Group LLC, an SEC Registered Investment Advisory and separate entity from LPL Financial LLC.

HSA Qualified Expenses May Include:

· Abortion

· Acupuncture

· Treatment for Alcoholism / Drug Addiction

· Ambulance

· Annual Physical Examination

· Artificial Limbs

· Artificial Teeth

· Bandages

· Birth Control Pills

· Body Scan

· Braille Books and Magazines

· Breast Pumps and Supplies

· Breast Reconstruction Surgery

· Capital Expenses (for special equipment for the purpose of your medical care)

· Car (specially designed to meet healthcare needs)

· Chiropractor

· Christian Science Practitioner

· Contact Lenses

· Crutches

· Dental Treatment

· Diagnostic Devices

· Disable Dependent Care Expenses

· Drugs

· Eye Exam

· Eyeglasses

· Eye Surgery

· Fertility Enhancement

· Founders Fee

· Guide Dog or Other Service Animal

· Health Institute

· HMO Premiums and Related Costs

· Hearing Aids

· Home Care

· Hospital Services

· Health Insurance Premiums (Including Medicare)

· Personal Protective Equipment

· Prepaid Insurance Premiums

· Laboratory Fees

· Lactation Expenses

· Lead-Based Paint Removal

· Learning Disability Costs

· Healthcare Related Legal Fees

· Lodging for Medical Care

· Long-Term Care

· Qualified Long-Term Care Contracts

· Meals At Healthcare Facilities (excludes weight-loss programs)

· Medical Conferences

· Nursing Home Costs

· Operations

· Optometrist

· Organ Donors

· Osteopath

· Oxygen Treatment

· Pregnancy Test Kit

· Prosthesis

· Psychiatric Care

· Psychoanalysis

· Psychologist

· Special Education

· Sterilization

· Smoking Cessation

· Surgery

· Special Telephone Equipment for Hearing Impaired

· Television For Hearing Impaired

· Therapy

· Transplants

· Transportation Essential to Medical Care

· Trips For Medical Purpose ($50/night Per Person)

· Weight-Loss Programs Prescribed by Physician

· Wheelchair

· Wigs Purchased Under Advice of Physician

· X-Ray Services